June 2013

CONSTRUCTION WORLD

20

Compared to certain segments

of the golf estatemarket in the

United States, South Africa’s

golf estate market overall

has fared somewhat better,

says Dr Andrew Golding, CE

of the Pam Golding Property.

property

“FROM 1990 TO 2003 SOME

3 000 new

courseswere built in theUnited States, boost-

ing the total number of courses nationally

by 19% and costing about USD20-billion,

according to the National Golf Foundation.

However, soon after that the sport began to

lose its allure and since 2005 over 350 golf

courses closed,”he says.

“Compounding the problem, some real

estate developers in the US had not consid-

ered the viability of the golf courses them-

selves. A number of these courses, designed

by brand-name golf course architects, were

championship level and too difficult for the

average player. They took a long time to play

and cost millions a year tomaintain, pushing

up annual dues. Across the country, about

2 000 of the 16 000 golf courses are‘financially

distressed’ and estimates are that 4 000 to

5 000 golf courses will be in financial danger

if they do not change their model. Some de-

velopers are recasting their golf communities

to appeal to a broader band of home buyers,

including more families and young people.”

Dr Golding says here in South Africa we

find both similarities and differences. He

says somewhat like the general residential

market, the South African golf estate market

is easily separated intometropolitan andnon-

metropolitan markets. “Consider Steenberg,

De Zalze and Atlantic Beach Estate in the

Cape, Mount Edgecombe, Zimbali and Sim-

bithi in KwaZulu-Natal and Dainfern, Silver

Lakes and Woodhill in Gauteng to name

but a few and you find these golf estates

are successful nodes in densely populated

residential suburbs. Froma property perspec-

tive, their performance has beenmore or less

recession-proof and actually very impressive,

especially when one compares property val-

ues in these estates to the surrounding areas.”

He says Zimbali and Simbithi are good

examples of this – both are significant estates;

Simbithi with1 800opportunities andZimbali

1 200. Ninety-five percent of both estates

are sold out, with Zimbali, being a more

mature development, enjoying 90%

completion of homes. Both are situated in

the Ballito area, where the total market sales

turnover in 2012 was R1,3-billion. Together,

Simbithi and Zimbali concluded sales in the

region of R800-million for the year, which is

two-thirds of the entire Ballitomarket. Of note

is that Simbithi land prices rose by 30-40%

since 2007, in themidst of a serious recession.

“Another excellent example of this typi-

cal golf estate ‘phenomenon’ is Cape Town’s

Steenberg Estate, which is listed as the

fifth most expensive place to live in South

Africa. There is a 540% difference in the aver-

age property value between a Steenberg

home and one that is just beyond its gate

in the suburb of Tokai. Similarly, De Zalze, a

380 erven estate, which has actually become

a suburb of Stellenbosch in the Cape Wine-

lands, has achieved consistent growth during

the quieter period since 2007 aswell as record

prices in excess of R20-million for individual

properties in 2008 and 2009,”says Dr Golding.

“Generally golf estates which are not

situated in or close to major metropolitan

areas have experienced more challenging

times. With the economic recession impact-

ing negatively on the purchase of holiday

homes, leisure destination golf estates came

under considerable pressure. Some estates

are simply too remote and not close enough

to metropolitan areas where statistically one

would find a higher demographic of wealth

to support not only the holiday home mar-

ket, but even just the estates’ amenities. The

hardest hit has been those inland or country

destinations which, during a recession, will

unfortunately take second place against

coastal property in the same category.”

Dr Golding says it appears that in South

Africa, the market for golf estate opportuni-

ties outside of metropolitan areas are limited,

not only from an availability perspective

but also in terms of the bulk infrastructure

contribution levies that are required upfront

by municipalities.

“For example, why should plots on golf

courses be so large? Is there any reason why

duplex style housing should not be devel-

oped around a municipal or public course

that has not been designed by a big name?

Perhaps we need to look for new opportuni-

ties in the golf property environment. An

excellent, up to the minute example is Steyn

City in northern Johannesburg, which will

provide 11 000 housing units, the best of

which are only on the perimeter of the new

golf course. The golf course itself greatly im-

proves the environment which is transformed

fromamixture of floodplain and quarry to an

Eden in comparison,”concludes Dr Golding.

●

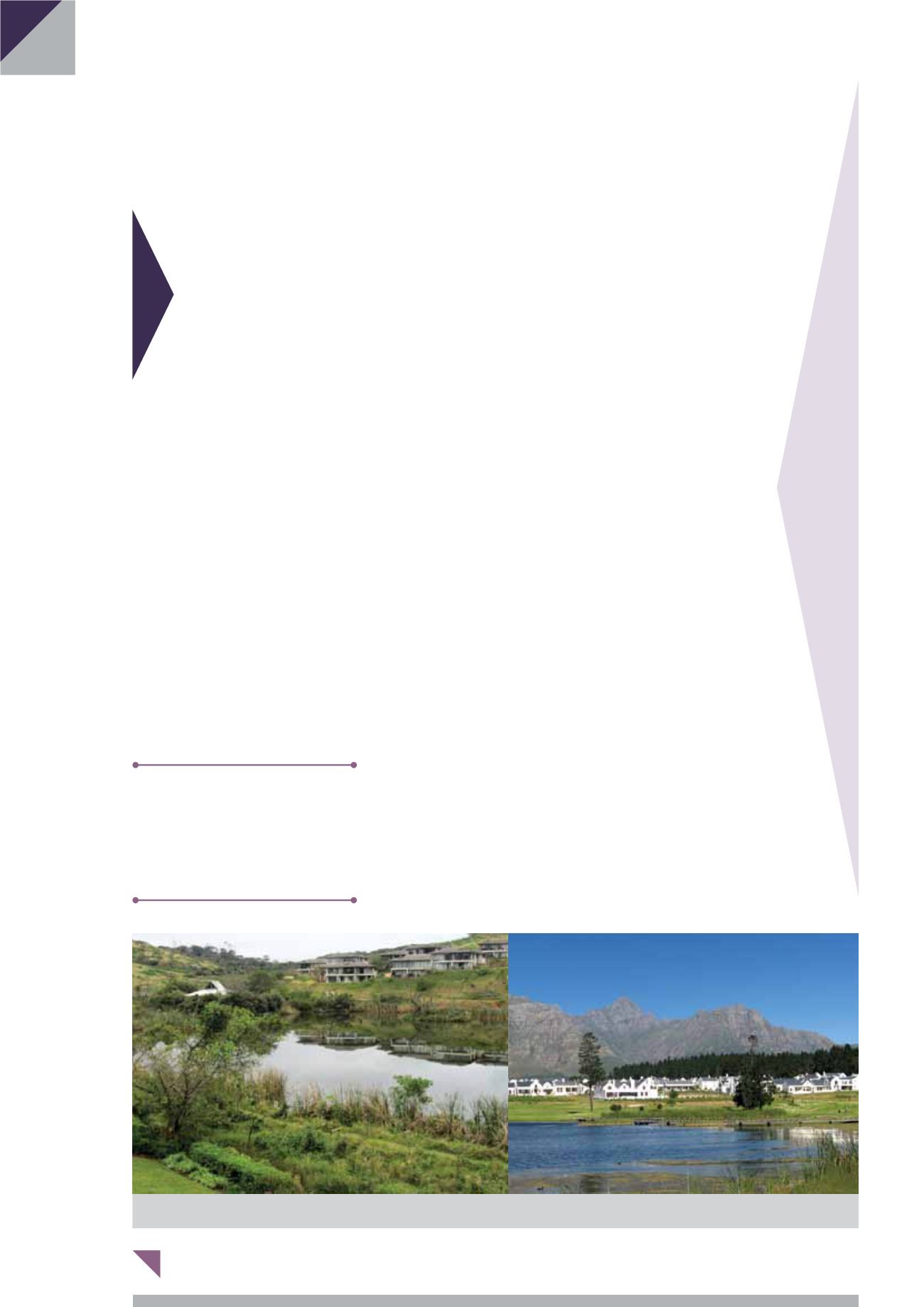

LEFT:

Simbithi in KwaZulu-Natal.

RIGHT:

De Zalze, a 380 erven estate, has become a suburb of Stellenbosch.

SA’s golf estate market has proven

relatively resilient

Together,SimbithiandZimbali

concluded sales in the region

of R800-million for the year,

which is two-thirds of the

entire Ballito market.