February 2014

MODERN MINING

31

COMPANIES

35 Level to 45 Level and, according to Mwana,

“secure the life of mine of the Trojan asset.”

Total (C3) cash costs increased during the

quarter from US$10 390/t to US$11 819/t, with

this being attributable to the continued pro-

duction ramp up and the re-deepening project.

Underground tonnage improved marginally

and should improve further with the imminent

delivery of two new LHDs to the mine.

Looking at the future of Trojan and the BNC

operation, Mpinga says that Mwana’s inten-

tion is to refurbish and restart the smelter and

refinery, which were originally built by Anglo

American in the 1960s. He says that the smelter

has the capacity to treat 175 000 t/a of concen-

trate. This capacity is far in excess of BNC’s

own requirements so there is a potential for the

smelter to be adapted to enable it to also handle

concentrate – potentially up to 100 000 t/a –

from Zimbabwe’s platinum producers, which is

currently being transported to South Africa for

smelting and refining.

Mpinga believes the refurbishing and reopen-

ing of the smelter (excluding the refinery) could

cost in the region of US$25 million but says the

savings on Mwana’s transport costs – currently

running at approximately US$1,2 million a

month – could see the project paying for itself

within two years. He adds that Hatch has been

retained to investigate the feasibility of bringing

the smelter back on line.

Further down the line, Mwana is also con-

templating recommissioning the Shangani

underground mine to the west of Gweru, which

has a resource of nearly 68 000 tonnes of nickel,

and developing the Hunters Road deposit north

of Gweru, where the resource totals 200 kt of

nickel at a 0,55 % grade. Hunters Road is mine-

able by open-pit methods with water, transport

links and power readily accessible.

While Mpinga is the driving force behind

Mwana, he has gathered around him a strong

team that includes one-time DRDGold CEO

Mark Wellesley-Wood as Non-executive

Chairman and James Arthur (whose previ-

ous posts include a stint as GM of Botswana’s

Mowana copper mine) as Executive VP –

Operations. Exploration is in the hands of

well-known geologist Charl du Plessis, pre-

viously responsible for African exploration

at AngloGold Ashanti, who is Executive VP

– Exploration, while Chris van Aswegen, pre-

viously GM at the Blue Ridge platinum mine

in South Africa, is VP – Mining and Projects.

David Murangari, with over 35 years’ experi-

ence in Zimbabwe’s mining industry (among

other things, he was Chief Executive of the

Chamber of Mines of Zimbabwe), runs BNC as

MD. At Freda Rebeccca, the MD is Toindepi

Muganyi, a graduate mining engineer with a

background in Botswana’s nickel/copper min-

ing sector.

Mwana Africa has disappointed in the past

but the company now seems to have a very real

prospect of emerging as a prominent player

in the junior to mid-tier mining market. With

over 5 Moz of gold and over 386 kt of contained

nickel in its portfolio, it clearly has an impres-

sive resource base when compared with many

of its peers. In addition, it has forged strong

strategic relationships with China International

Mining Group Corporation (CIMGC), Hailiang

(its JV partner in Katanga on its copper licences)

and Glencore. Add to this its solid operational

or near operational assets (in the form of Freda

Rebecca, Trojan, Shangani and the smelter/

refinery complex) and the future looks good for

the company. But mining is an uncertain game

and it will be interesting to revisit Mwana in a

year or two to see what success it is having in

realising its undeniable potential.

Report by Arthur Tassell, photos courtesy of Mwana Africa

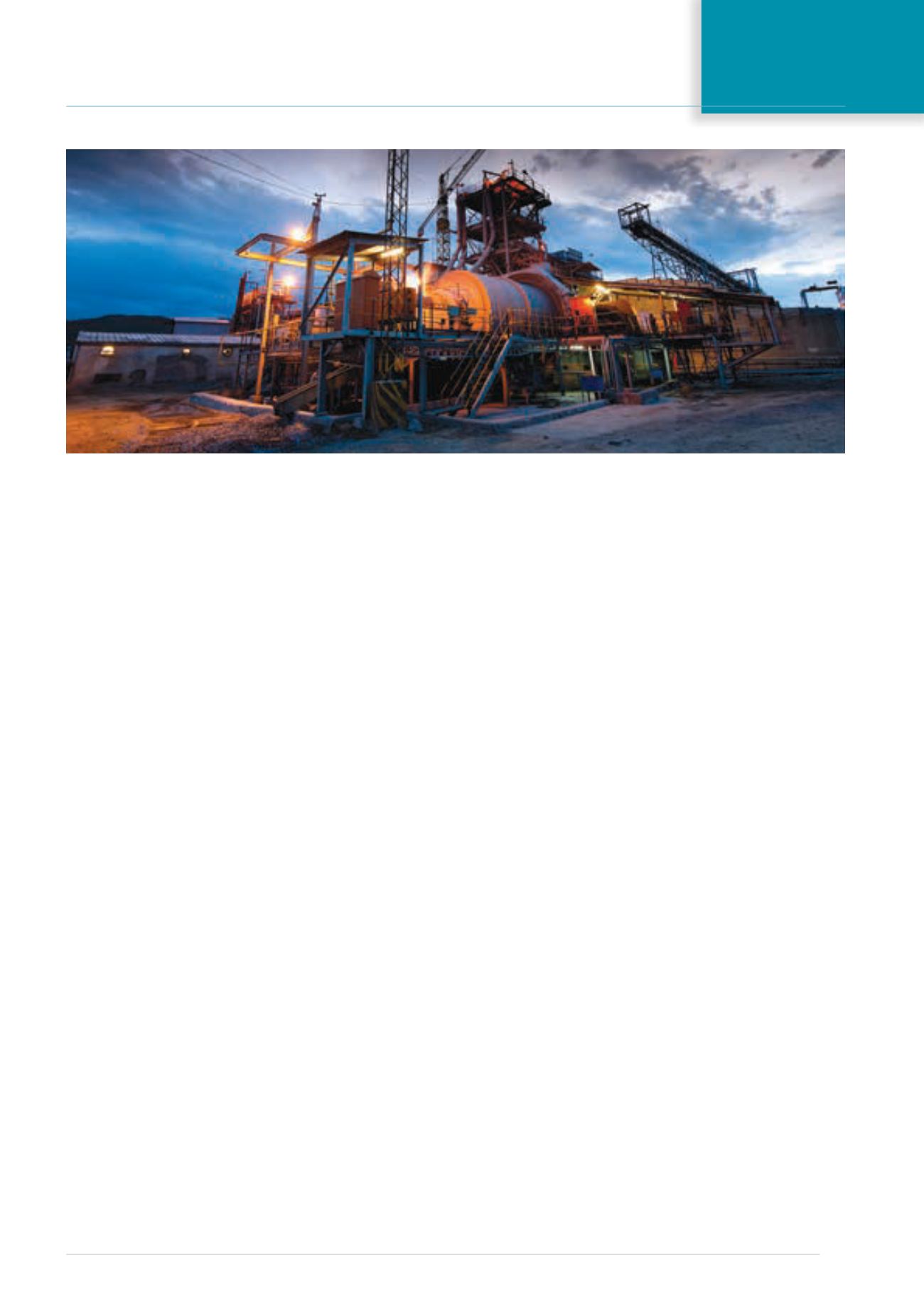

Another view of Freda

Rebecca’s metallurgical

plant. In the six months to

30 September 2013, the

mine produced 45 324

ounces of gold.