South African consumers may be feeling the pinch following a further two interest rate hikes in the first quarter of 2023, but ooba Home Loan’s Q1 2023 oobarometer indicates that there are still opportunities in the property market.

The latest data released by the country’s leading home loan comparison service indicates that homebuyers continue to take advantage of the competitive lending environment and attractive interest rate discounts offered by the country’s major banks.

Rhys Dyer, CEO of ooba Home Loans elaborates: “With interest rates now close to peaking, growth in property prices remaining subdued relative to household earnings and the continued willingness of banks to extend credit to homeowners, conditions remain favourable for those with a long-term view to property purchase.”

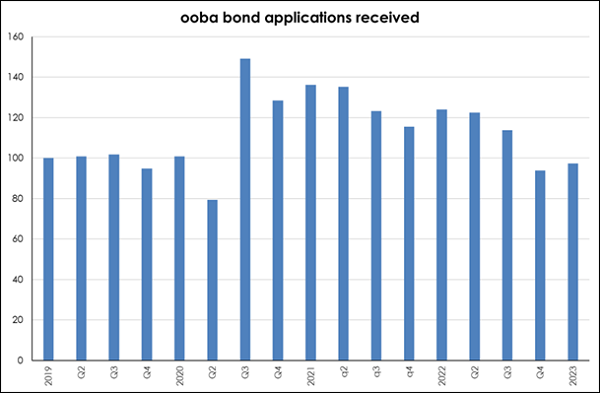

Application volumes resemble pre-COVID levels

“However, while the market remains competitive and has recorded steady activity levels in the first quarter of 2023, multiple recent interest rate hikes have had a dampening impact on consumers whose disposable income is coming under pressure,” he continues.

This is evident in the drop in home loan application volumes observed by ooba Home Loans, aligning to the accelerated series of rate hikes that began in November 2021 and have bumped up the prime lending rate from 7% to its current level of 11.25%.

“Application volumes recorded in Q1 ‘23 are down 20% from Q1 ‘22 and the value of our instructed bonds are down by the same percentage from Q1 ‘22,” comments Dyer. “However, the good news is that the current application volumes resemble those received in Q2 and Q3 ‘19 (when prime was 10%), leading us to believe that this dip is part of the natural interest rate cycle.”

Homebuyers attracted to lower property prices

Q1 ‘23 saw a national average purchase price of R1 434 448 - up by only 0,8% from R1 422 992 in Q4 ‘22. For the same period, the first-time buyer segment recorded an average purchase price of R1 136 625 – an increase of just 0.4% on Q1’22.

While this sideways trend may be of concern to those wishing to sell in the near future, Dyer believes that it is good news for prospective homebuyers who have been waiting for the right time to enter the market. “Slowing house price inflation (HPI) means that properties are becoming more affordable, relative to household incomes.”

Looking to regional property price trends, the average purchase price across the country remained relatively stable, barring Kwa-Zulu Natal where prices continue to rebound after a difficult last quarter. “Following the province’s 7.01% year-on-year growth in 2022, the Eastern Cape has also lost some of its momentum with an average purchase price of R1.46 million in Q1 ’23 – down from R1.73 million in December ‘22,” says Dyer.

Regions such as the Free State, Gauteng South & East and Mpumalanga recorded the country’s lowest average purchase price and are stimulating some much-needed activity amongst first-time homebuyers. “Free State comes out on top for first-time homebuyer applications in Q1 ‘23 – sitting at 71.4%, followed by Mpumalanga at 59.4%.”

The Western Cape retained its top spot with the highest average purchase price of R1.81 million, followed by Gauteng North & West at R1.5 million.

Salaries growth outpaces house price inflation

The nine consecutive interest rate hikes since late 2021 has resulted in monthly bond repayments – as a percentage of gross income – rising from a low of 18.3% in Q3’21 to a high of 20.2% in Q1’23.

At a national level, gross earnings have risen at a faster pace than house prices. According to StatsSA, average monthly earnings have risen by 22.6% between Q1’19 and Q1’23 while the average purchase price of homes has risen by 16.1%.

Property buying activity robust at the middle to higher end of the market

60% of finally granted bonds in Q1’23 fell into the price segment above R1.5m, up on the 58% recorded in Q1 ‘22, while properties in the price range above R750,000 to R1.5 million account for 30% - compared to the 31% recorded in Q1 ‘22. 10% of finally granted bonds in Q1 23 fell into the price category below R750,000, down 1% on Q1 ‘22. “Despite the accelerated pace of interest rate hiking since November ’21 there has been no significant shift yet towards the lower purchase price segments” notes Dyer.

Western Cape driving the buy-to-rent boom

Applications for buy-to-rent properties has risen nationally in recent years, now accounting for 8.3% of the applications received nationally in Q1’23. “Initially triggered by the low interest rate environment and increased demand for rental and student properties, this is the highest percentage of home loan applications that we have received since late 2009.”

When looking at regional trends it is clear that demand for investment and buy-to-rent properties is primarily driven by the Western Cape, where applications have risen to 22.8% in Q1’23 – exceeding the pre-Covid high of 21.5% in Q1’20. “This is presumably attributable to the current wave of semigration to the Western Cape as well as the view that Western Cape property properties are generating stronger rental yields,” adds Dyer.

Deposits trending upwards

A 11.9% year-on-year increase now pins the average home loan deposit at a sizeable R107 268 (Q1 ’23) - averaging 7.5% of the total purchase price. “Savvy homebuyers continue to prioritise deposits to help bring down their monthly repayments and secure the best interest rate in a tough economy.”

Q1 ’23 statistics for first-time homebuyers also reveal an average deposit of R109 793 (9.7% of the purchase price), marking a whopping 44.8% year-on-year increase and a 10.2% increase from Q4 ‘22.

“We are pleased to see this market segment embracing deposits as a sign of smart financial planning,” adds Dyer.

Attractive prime lending rates supports home buying activity

In a high interest rate environment, achieving a lending rate below prime is an essential cost-saving tool. Luckily for homebuyers, the country’s major banks are continuing to compete for home loan market share with competitive pricing.

ooba Home Loans achieved an average interest rate of prime less 0.45% for its customers over this period - a significant improvement on the average rate achieved in Q1 ’22 of prime less 0.23%.”

Elevated bank approval rates prevail

Nationally, the banks’ approval rates remain steady and ooba Home Loans achieved an 82.9% approval rate for its customers in Q1 ‘23. “This marks a 0.6% increase from Q1 ‘22 and evidences the continued confidence by home loan lenders in the property market,” he adds.

“Interestingly, 90.4% of our homebuyers who availed themselves of our pre-qualification services were approved in Q1 ’23, once again highlighting the importance of being pre-approved prior to shopping around. Pre-qualified homebuyers also have the upper hand when it comes to negotiating the terms and cost of the property with sellers.”

“While a higher interest rate environment is not without its challenges, the sustained slow growth in property prices coupled with rate discounts on home loans and availability of financing means that there are still plenty of good investment opportunities to be found in South Africa’s residential property market” concludes Dyer.