AIM-listed coal miner MC Mining has provided an update for its activities, including the Limpopo projects: Makhado hard coking coal project, Vele Colliery and Greater Soutpansberg Projects (GSP).

Makhado Project Update

MC Mining announced the completion of the Bankable Feasibility Study (BFS) for its fully licenced, shovel ready (subject to further funding) Makhado Project, on 13 April 2022. The BFS was prepared by Minxcon ( (Minxcon), an independent mining industry consulting firm, and is a key milestone in securing the funding for the Project. Seeking to unlock near-term shareholder value, the ‘Base Case’ development plan in the BFS was designed to minimise the upfront capital expenditure by utilising the existing Vele Colliery infrastructure, as this mine currently remains on care and maintenance.

The Base Case BFS produced favourable financial results. Following the BFS, Minxcon was commissioned to assess potential alternative development scenarios for Makhado. This assessment was completed with a view to optimise capex and reduce operational costs at Makhado, including possibly:

- moving the Vele CPP and modifying this at Makhado; or

- the construction of a bespoke CPP at Makhado.

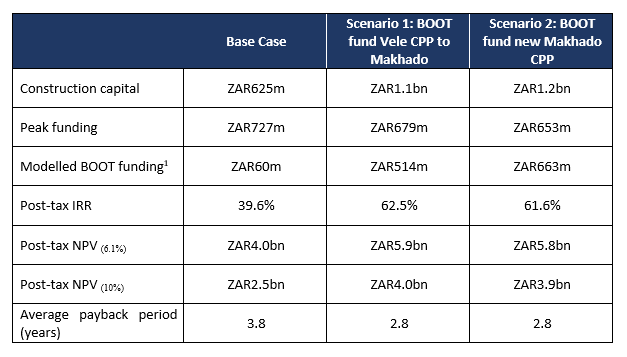

Both additional development scenarios were developed to pre-feasibility level and would result in the mining of the East Pit, followed by the Central and West Pits and the hauling of saleable coal only 72km from Makhado to the Musina siding. These two scenarios would require additional capital expenditure but would significantly reduce the transport costs when compared to the Base Case scenario. While the BFS Base Case is feasible and economically robust, the additional two scenarios resulted in improved project economics. These are detailed in the table below.

Both of the alternative scenarios result in a significant value improvement to Makhado compared to the Base Case, with increased NPV and IRR values. This is primarily due to reduced transportation costs over the LOM, which improves operational margins and generates long-term value for shareholders. Whilst the peak funding requirements for both scenarios are higher, the payback periods are slightly shorter due to the lower operating costs.

The option of moving the Vele CPP provides the most attractive financial metrics but removes the Vele asset from MC Mining’s portfolio and limits future exploitation of the Vele Colliery. The construction of a new plant at Makhado provides similar results but requires additional peak funding of ZAR145m while also keeping the Vele CPP intact for future exploitation. The increased peak funding requirement for both scenarios resulted in Minxcon assessing the option of reducing the Makhado peak funding requirements through a build, own, operate, transfer (BOOT) arrangement.

The BOOT (pre-feasibility level) funding options significantly reduce the funding requirement of both alternatives:

- Scenario 1: BOOT funding of ZAR514m reduces the peak funding of moving the Vele CPP from ZAR1.2bn, to ZAR679m.

- Scenario 2: BOOT funding of ZAR663m reduces the peak funding for the construction of a new Makhado CPP from ZAR1.3bn, to ZAR653m.

The NPV values for both scenarios remain similar but the internal rates of return (IRR) increased significantly - from 45.2% to 62.5% for the move Vele CPP option and from 41.0% to 61.6% for the new Makhado CPP option. Accordingly, the new Makhado CPP option utilising a BOOT financing arrangement is considered to be the preferred option as it provides similar results while keeping the Vele CPP intact for future exploitation of that Coal Resource. Furthermore, both alternative scenarios improved the Makhado Project’s economics due to the lower operating costs achieved. Further, the Project’s Coal Reserve base and LOM should increase following further study work as deeper material becomes available.

As a result of this pre-feasibility exercise, MC Mining has initiated discussions with potential BOOT funding providers..

Vele Colliery

The Vele Coal Resource comprises both semi-soft coking coal (SSCC) and export quality thermal coal. However, the Vele’s CPP does not have the requisite fines circuits that would allow for the simultaneous production of SSCC and thermal coal. The Company has previously reported that due to the global economic downturn and lower coal prices, the colliery was placed on care and maintenance from August 2013.

The option of building a CPP at Makhado has resulted in the assessment of potential alternative exploitative scenarios for the Vele Colliery. The previously envisaged phased approach to the development of Makhado Project would have resulted in the processing of Makhado’s crushed and screened coal at the Vele CPP which would have required modifications to the Vele CPP of approximately ZAR397m.

The improved market conditions and construction of a new CPP at Makhado creates optionality for the potential recommencement of operations at Vele.

Godfrey Gomwe, CEO, commented:

“MC Mining has made very pleasing progress during the last four months. This includes securing the standby loan facility which ensured the Company had sufficient liquidity while it builds-up inventory prior to accessing international thermal coal markets. This has been achieved by reaping the benefit of coal prices which remain favourable due to geopolitical events and the global energy shortage.

The company has also enhanced the Makhado Bankable Feasibility Study, ensuring we have assessed opportunities to maximise the Project’s economic returns. Once developed, Makhado is expected to be South Africa’s pre-eminent coking coal mine and would replace a significant amount of imported hard coking coal. MC Mining continues to explore potential marketing strategies for Makhado’s coal while the composite funding package for the development of the Project is being concluded. We are planning to commence with certain early-works activities at Makhado later in CY2022 and funding dependent, construction is planned to commence in early CY2023.”