Lux Research has released an analysis of how future global energy networks will evolve as a result of the move away from carbon-based fossil fuels. Lead analyst, Tim Grejtak, presents key findings.

Click to download and read pdf

Today’s global economy is enabled by the global energy trade, with countries around the world dependent on flows of oil, coal and natural gas to keep their economies growing.

As countries move to decarbonise and adopt renewable energy, many are finding it difficult to do so cost-effectively because of fundamental limitations in solar and wind resources. For these countries to fully decarbonise without breaking the bank, they must develop innovative renewable energy carriers and build new zero-carbon energy supply chains.

In a new report, Evolution of Energy Networks: Decarbonizing the Global Energy Trade, Lux Research examines these renewable energy carriers and the countries and companies developing them.

Not every country in the world can satisfy its demand for energy from domestically produced renewable sources. Some countries simply lack the land area and resource potential to power their energy-intensive economies.

“Places such as Singapore, Japan and the Netherlands are great examples of countries that cannot meet their energy demands solely through domestic renewable sources like wind and solar energy,” says Grejtak, Lux Research analyst and the lead author of the report. “In fact, countries representing US$9-trillion of global GDP cannot meet their energy demands solely through domestic renewable energy production and will require the import of renewable energy from more resource-rich countries,” he explains.

To achieve their decarbonisation goals, these countries will need to find ways to import zero-carbon energy. Some of the ways identified for doing this include:

- Building new electricity infrastructure using high-voltage ac or dc transmission lines as a primary means of importing low-cost solar energy from distant regions.

- Power-to-gas technology using pipelines is limited and shipping liquefied hydrogen, methane or ammonia offers better economics, but only over long distances.

- Imported energy costs can be competitive against other zero-carbon technologies, but no energy carrier can offer costs low enough to replace LNG or oil and offer a global renewable energy trade.

Not only is the demand for energy imports growing; it is also diversifying. New energy carriers such as liquefied natural gas (LNG) tankers are supplementing or, in some cases, substituting the traditional oil and coal vessels that have largely made up the mix of energy imports to date.

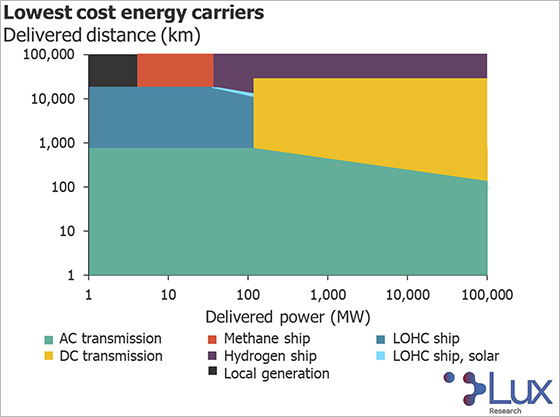

“Our analysis shows the expanded buildout of ac and dc powerlines will be the most cost-effective way of importing low-cost solar energy from distant regions, though only up to roughly 1 000 km. At farther distances, other renewable energy carriers such as synthetic fuels are less expensive. It’s important to note that imported energy costs can be competitive against other zero-carbon technologies, but no current energy carrier can offer costs low enough to completely replace liquid natural gas (LNG) or oil,” Grejtak adds.

Delivering energy via land-based powerlines or pipelines becomes expensive at long distances because of the inefficiencies of powerlines and the capital costs of pipelines. Delivery via ship, on the other hand, is much more cost-effective at long distances, whether it be LOHC delivered by tanker or liquid hydrogen delivered using cryogenic carriers like those used for LNG.

Crucially, Lux’s analysis found that across all renewable energy carriers, low-cost solar energy can be delivered to resource-constrained regions at 50% to 80% lower costs than generating that solar energy locally under less favourable conditions. This value proposition will motivate the construction of billions of dollars of new infrastructure in countries committed to reducing their carbon intensity.

The report evaluated the lifetime costs of 15 different renewable energy carriers ranging from conventional carriers, including electricity, hydrogen, synthetic methane and ammonia; to more advanced carrier concepts such as liquid organic hydrogen carriers (LOHCs), vanadium and aluminium.

Specific energy carriers will dramatically reshape how particular regions access low-cost renewable energy. Combinations of liquid organic hydrogen carriers, high-voltage dc transmission and liquefied hydrogen are expected to enable energy-intensive economies to reach their CO2 targets from 2030.

The report notes that:

- Successful projects will target multiple high-value applications and industry consortia will be key.

- Focusing on difficult-to-decarbonise sectors such chemicals, heavy transportation and heat will make better use of energy carriers. These sectors intersect around industry and partnerships among industry, logistics and renewable power generators will be essential.

- New infrastructure projects are not cheap and consortia are critical in order to reduce and share costs. These renewable energy carrier projects will cost of billions of dollars each and such costs cannot be borne by industry alone; governments will also have to play a role.

- A common global renewable energy trade is unlikely. Even with highly favourable conditions, high-volume energy carriers can only just match LNG prices today. If renewable energy displaces hydrocarbons, though, future LNG prices will be lower as demand drops.

Lux predicts the first tipping point for deploying renewable energy import infrastructure will be in 2030, when imported electricity via new HVDC power lines becomes cheaper than low-carbon natural gas turbines. The next tipping point will occur in 2040, when imported liquid hydrogen becomes cheaper than low-carbon steam methane reformation. This gives companies today just 10 years to develop the partnerships and pilot projects necessary to demonstrate such a transformative energy paradigm.

Major companies, including Kawasaki Heavy Industries, Mitsui & Co, Equinor and Shell are already developing their own decarbonised energy trade routes in Europe, Japan, and Southeast Asia, meaning the fight for $500-billion of energy imports in those regions is just beginning.

The executive summary of the report can be downloaded by clicking here…