Metals Focus, a leading independent precious metals consultancy, has announced the publication of Gold Focus 2026, its flagship annual report offering a comprehensive analysis of the global gold market.

This year’s edition features comprehensive historical supply and demand data from 2017 to 2025, as well as a detailed forecast for 2026.

Outlook for 2026:

- Gold Supply: Modest growth in both mine production and recycling is expected to lift total supply by 3.1% in 2026.

- Gold Demand: Total demand is projected to decline by 2.3%, as double-digit losses in jewellery and central bank purchases are largely offset by stronger physical investment (coin and bar demand). This is set to replace jewellery as the largest component of demand for the first time.

- Price Outlook: Despite short-term headwinds from the Iranian conflict, gold is expected to resume its bull run once the war concludes. The annual average gold price is forecast to surge by 43% to a new record high of $4,920 in 2026.

Highlights of the Gold Focus include:

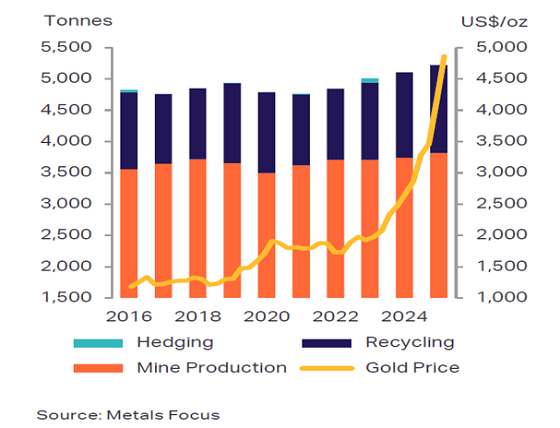

- Mine Supply: Global gold mine production reached another high in 2025, rising 2.0% year-on-year (“y/y”) to 3,817 tonnes (”t”), driven by new mines, expansions, and higher artisanal and small-scale gold mining. Global all-in sustaining costs rose by 12% y/y to $1,552/oz, underpinned by higher royalties and inflationary cost pressures. In 2026, gold mine supply is forecast to increase again, by 2.4% y/y to 3,907t, as output strengthens in all regions except for Oceania and Europe.

- Recycling: Global recycling rose by just 2.8% y/y in 2025, albeit to a 13-year high of 1,404t, despite gold prices setting comfortable record annual averages. This performance was driven by gains in Europe, as well as modest increases in most other regions, all of which offset notable weakness in South Asia. Scrap supply is forecast to rise by 5.1% y/y in 2026, as low near market stocks and the desire to retain gold as a safe haven limit gains despite sharply higher prices.

- Official Sector: Net official sector purchases fell by 22% y/y to a four-year low of 848t. Buying was spread geographically, as elevated US policy uncertainty encouraged further diversification. Sales were concentrated among a small number of countries, largely reflecting portfolio rebalancing after the price rally. Despite headwinds from the energy shock, net purchases are expected to remain historically high in 2026 as diversification-led drivers persist.

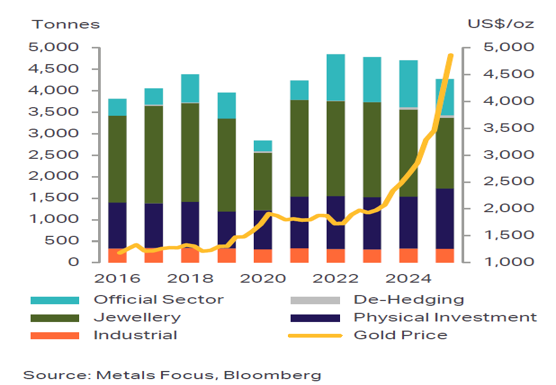

- Investment: Exchange-traded product (ETP) holdings rose by 803t in 2025, marking the highest annual inflow since 2020 with gains being widespread. Tariff uncertainty, rising US debt, concerns over Federal Reserve independence, and ongoing geopolitical turmoil all enhanced gold’s investment appeal. Physical investment rose 16% to a 12-year high, as strong price gains fuelled retail demand.

- Industrial: Electronics demand was effectively unchanged in 2025 as gains from the expansion of AI infrastructure were offset by weakness in consumer electronics. Decorative and Other Industrial fabrication contracted by 4.9% in 2025, to its lowest level since a pandemic-affected 2020.

- Jewellery: Global jewellery fabrication fell sharply in 2025, by 19%, to a five-year low of 1,646t. Most countries saw losses, as high prices dominated the trend, prompting light-weighting, carat shifts and some substitution from gold to platinum and plated or gold-filled jewellery. In 2026, the decline is expected to continue, by a further 11%, leaving fabrication only slightly above a pandemic-impacted 2020.

Extract from the report: “Gold’s fundamentals were a mixed bag last year. Mine production rose by 2.0% y/y to a record 3,817t, supported by new ramp-ups, expansions and stronger ASGM activity. Recycling increased by only 2.8%, in spite of the 44% rise in the average gold price and even stronger gains in local prices for some key markets, as bullish sentiment and limited near-market stocks restrained selling.

On the demand side, jewellery fabrication remained under heavy pressure because of higher prices, with India and China leading losses. By contrast, physical investment rose by 16% to a 12-year high, reflecting bullish price expectations and concerns about heightened economic and geopolitical uncertainty.

“Shifting to 2026, as noted earlier, the year started on a positive note, with fresh all-time records achieved in January. Changing expectations on US policy rates and the fact that the market had become overbought fuelled a correction soon after. The war in Iran has also added pressure to the gold price, as concerns about inflation have further reduced the scope for US rate cuts and boosted sovereign yields and steepened curves.

In spite of these headwinds, we are confident that, once the Iran war dust settles, gold will resume its bull run. This is premised on our expectation that the worst will be avoided and that, on balance, policy-makers will tolerate elevated inflation, rather than sacrifice growth. Crucially, all other factors that underpinned gold last year discussed earlier in this introduction are likely to remain in place over the rest of 2026 and beyond.”

Matthew Piggott, Director of Gold and Silver at Metals Focus, commented:

"Gold rallied strongly in 2025, by 44%, its best performance since 1980. Although net central bank purchases were roughly a fifth lower than the year before following three consecutive years of 1,000 tonnes plus gold demand, the 2025 figure remained significantly above pre-2022 levels, with the official sector continuing to play a strategic role in the gold market.

"A further shift by consumers away from jewellery, in favour of bars and coins, also contributed to last year's dynamic, with China (+28%) and India (+17%) leading the gains. For the first time in our series, physical investment is set to replace jewellery as the largest component of gold demand.

"More recently, losses following the January rally and range-bound prices have disappointed many individual investors, and a number of key bar and coin markets have been hit hard by high oil prices, eating into disposable incomes. That said, the drivers from 2025 remain intact: ongoing US policy uncertainty, persistent concerns about the dollar's long-term outlook, elevated geopolitical risks, and stretched equity valuations. Together, these factors reinforce gold's role as a safe haven and portfolio diversifier, and we expect further all-time records to be achieved later this year.

Figure 1: Global Gold Supply

Figure 2: Global Gold Demand

Figure 3: Jewellery Consumption & Physical Investment