Mechanical Technology — February 2014

33

⎪

Innovative engineering

⎪

Envisaged market

structure.

proposed carbon tax

to note that offset trading can be used

in a number of regulatory regimes, and

that the work in the project is, therefore,

also applicable to a broader suite of

policy instruments or measures. Some

examples are:

Cap-and-trade: This is the traditional

application of offset trading. In such

a scheme offsets can be used to meet

an emitter’s commitment towards its

emissions cap.

Tax-and-trade: the proposal in this

report.

Carbon budget: Under such a

scheme an offset can be bought in

the market and used towards the

obligation of an emitter to remain

within a predefined carbon budget.

The role and impact of offsets is dem-

onstrated opposite. In this example a

company emitting 100 t has a tax liabil-

ity of R4 800 after taking the tax-free

threshold of 60% into consideration.

The company now buys 10 t of offsets

at a price of R80/t, and thereby reduces

its tax liability to R3 600 (10% of the

taxable 40%). The overall saving due to

the purchase is R400, which represents

8,3% of the original tax liability.

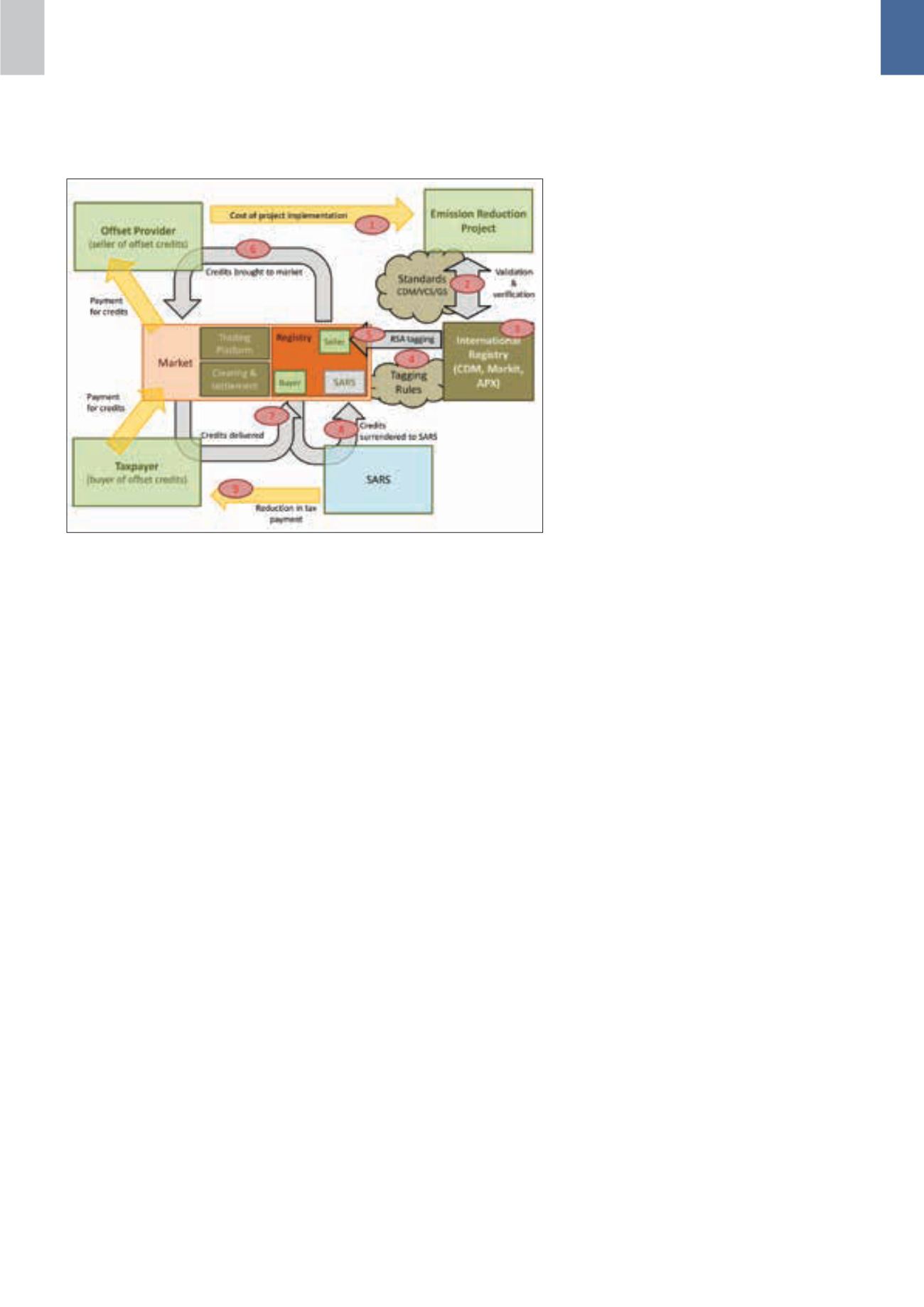

How the market would

function

A possible market structure is shown in

above. Nine process steps are indicated

and summarised below:

1 The offset provider invests in an

offset project. This project can be

either inside the business of the

offset provider or outside.

2 The project is validated and veri-

fied by an accredited auditor of the

standard used (CDM, VCS, GS). This

process guarantees the environmen-

tal integrity of the system.

3 The credits generated by the project

are issued into an international reg-

istry in terms of the scheme under

which the project was developed, eg,

the CDM registry for CDM projects or,

for VCS or GS projects, either Markit

or APX registries could be used.

4 The owner of the credits can now

apply for the credits to be transferred

to the South African Scheme. This

is done by auditing the credits for

national appropriateness according

to the RSA tagging rules. This audit

could be done by the project auditor.

5 The credits are issued into the ac-

count of the offset provider in the

RSA registry against delivery of the

tagging audit report and the cancel-

lation certificate from the registry of

origin.

6 Once the credits arrive in the ac-

count of the offset provider, he can

bring the credits to the market to be

traded.

7 The taxpayer buys the credits on the

market. The credits are transferred

to the registry account of the buyer.

8 The taxpayer surrenders the credits

into the cancellation account of the

South African Revenue Services

(SARS).

9 The taxpayer receives a reduction in

his tax liability that is equal to the

CO

2

value of the surrendered credits.

The following project participants and

their subsequent roles can be distin-

guished:

The offset provider implements an

emissions’ mitigation or carbon

offset project.

An accredited auditor is required

during the project validation phase in

order to ensure environmental integ-

rity of the carbon offset. Currently this

competency is either confirmed by

the UNFCCC, under the ISO14065

standard, and since 2013, locally

through SANAS. Local accreditation

could bring the cost of auditing down,

while creating jobs and building ca-

pacity in the green economy.

The Designated National Authority

(DNA): This report proposes to use

the chair of the custodian committee

of the SA tagging rules for the DNA

role. The DNA gives host country

approval to offset projects.

The tax payer/carbon emitter: Once

the offset provider has brought off-

sets to the market, the taxpayer can

purchase these offsets and surrender

them into the cancellation account

of SARS.

The South African Revenue Service

(SARS): upon receiving the offset

credits from the taxpayer, SARS

deduct these offsets from the total

carbon tax liability of the taxpayer.

Conclusions

As credible international standards,

such as CDM, VCS and the Gold Stan-

dard exist, it is recommended these be

used, especially during the implementa-

tion phase.

Reliable trading infrastructure,

through the JSE, for example, is

available within South Africa and will

require minimum modifications and

investments. Interviews with both in-

ternational, as well as local registries

found both to be available and suitable

for maintaining records of the ownership

of credits in the trading system.

Offsets have the potential to reduce

business as usual emissions by ap-

proximately 3% by 2020, which is

10% of South Africa’s 34% emmision

reduction target.

.